There are three key ingredients that can lead to success for the prudent investor.

• Diversification. A diversified strategy captures the compensated risk dimensions of the markets in the most reliable fashion. Exposure to three equity risk factors and two fixed income risk factors accounts for most of a diversified portfolio's expected return. The three equity risk factors are:

- Market—stocks have higher expected returns than fixed income securities.

- Size—small cap stocks have higher expected returns than large cap stocks.

- Value—lower-priced “value” stocks have higher expected returns than higher-priced “growth” stocks.

Two additional risk factors reflect compensated risk in the fixed income markets. These are:

- Maturity—longer-term bonds are riskier than shorter-term bonds.

- Credit—bonds of lower credit quality are riskier than bonds of higher credit quality.

Equities have offered a higher expected return than fixed income, but these stronger premiums come with higher risk. Structuring a portfolio around compensated risk factors can change many aspects of the investment process. Rather than focusing on individual stock or bond selection, investors work to achieve diversified, controlled exposure to the risk factors that drive expected returns.

An investor first determines his portfolio’s stock/bond mix, and then decides how much additional small cap and value to hold in pursuit of higher expected returns. The level of risk assumed in the fixed income component may depend on why an investor is holding fixed income. For example, an equity-driven investor who wants to reduce portfolio volatility may hold less risky debt instruments, while an investor pursuing higher yield or income may take more maturity and default risk.

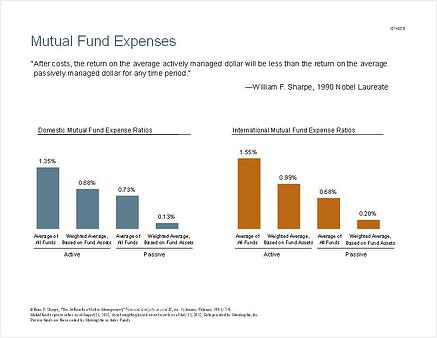

• Low costs. Management fees, trading commissions, market impact costs, bid/ask spreads, administrative expenses, and sales commissions (if any) directly reduce net investment returns. The combined effect of these costs can be difficult to compute and can consume a surprisingly high proportion of the gross investment returns offered by the capital markets.

In both US and non-US strategies, the average actively managed mutual fund is considerably more expensive than the average passively managed fund.

The graph compares average expense ratios of actively managed funds to those of passive funds. The ratios are presented as simple averages and weighted averages. The weighted average calculation indicates that larger funds tend to have lower expenses than smaller funds.

Active managers, on average, charge more than twice the fees of passive managers. This is also true in the international fund universe, although the differences are not as large due to the higher costs of investing in non-US markets.

Nobel laureate William Sharpe has pointed out that active management in aggregate must underperform passive management, not due to controversial financial theories but by the simple laws of arithmetic.

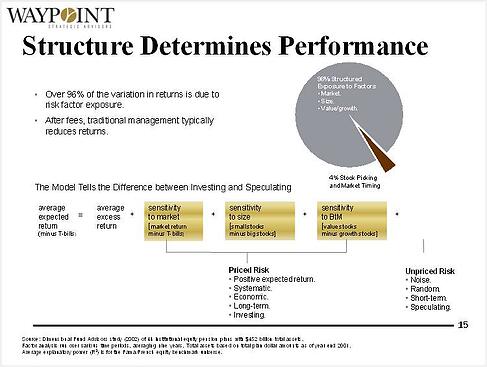

• Disciplined policy. Portfolio structure is the key determinant of results. 96% of portfolio performance is determined by structure and the discipline to stick to it, not stock picking or market timing (4%). The principal challenge for investors is to develop an asset allocation policy that matches an investor's risk preferences with returns offered by the capital markets. A successful policy is one that can be adhered to without anxiety in both good and bad markets.

Structuring a portfolio around compensated risk factors can change priorities in the investment process. The focus shifts from returns chasing (through stock picking or market timing) to diversification across multiple asset classes in a portfolio.

The model in this slide illustrates this multifactor approach. Investors receive an average expected return (above T-bills) according to the relative risks they assume in their portfolios. The main factors driving expected returns are sensitivity to the market, sensitivity to small cap stocks (size factor), and sensitivity to value stocks (as measured by book-to-market ratio). Any additional average expected return in the portfolio may be attributed to unpriced risk.

Let us show you how diversification, low cost and a disciplined policy can help you achieve your investment goals while sleeping soundly at night.